If you're exploring an Online Mutual Fund Investment Platform in Mumbai, chances are you’ve come across two options: Direct and Regular mutual fund plans. At first glance, they look similar. Same fund, same portfolio, same fund manager.

But here’s the thing: the difference lies in how you invest and how much you earn over time.

What Are Mutual Fund Plans?

Mutual funds pool money from multiple investors and invest in stocks, bonds, or other assets. But how you access these funds creates two versions:

What is a Direct Plan?

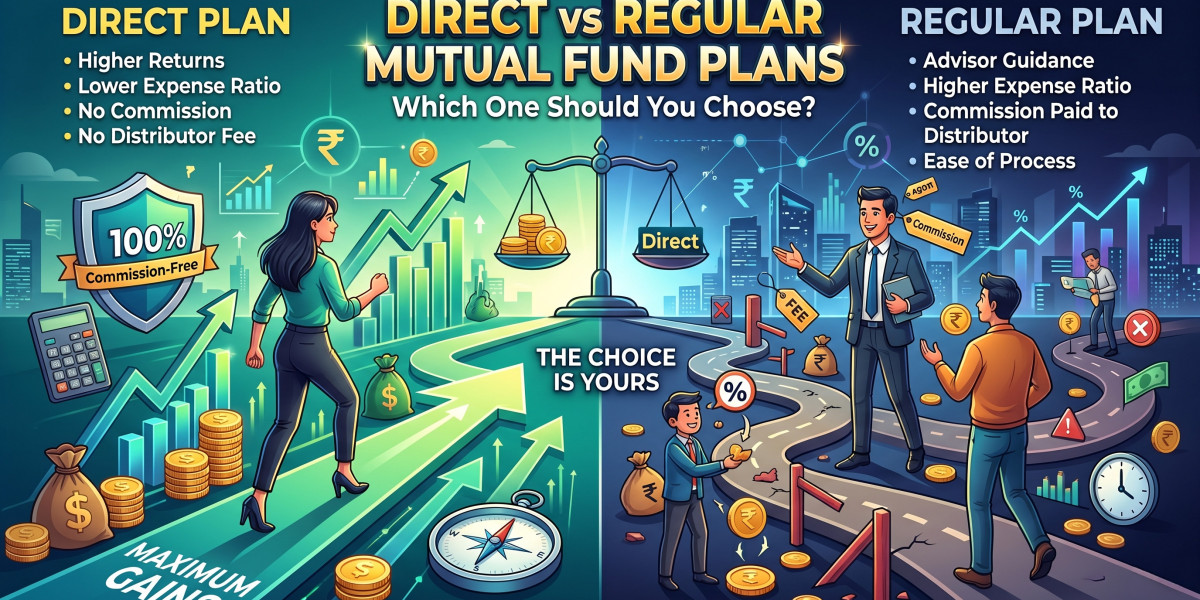

A direct mutual fund plan is when you invest directly with the fund house (AMC) no intermediary involved.

- No broker or advisor commission

- Lower expense ratio

- Higher long-term returns

What is a Regular Plan?

A regular mutual fund plan is when you invest through an intermediary like an agent, bank, or distributor.

- Includes commission fees

- Higher expense ratio

- Offers advisory and guidance

Key Differences Between Direct and Regular Plans

| Factor | Direct Plan | Regular Plan |

|---|---|---|

| Investment Mode | Direct with AMC | Through a broker/distributor |

| Expense Ratio | Lower | Higher |

| Returns | Higher (due to lower cost) | Slightly lower |

| Advisory | No | Yes |

| Control | High | Moderate |

Expense Ratio: The Real Game Changer

This is where things get interesting.

The expense ratio is the annual fee charged by the fund. In regular plans, this includes distributor commissions.

Even a 1% difference can significantly impact your wealth over time.

Example:

- ₹10 lakh invested for 20 years

- Direct plan could generate ₹5–10 lakh more than a regular plan

What this really means is small costs today can quietly eat into your future wealth.

Returns Comparison: Direct vs Regular

Over time, direct plans outperform regular plans.

Why?

Because the money saved on commissions stays invested and compounds.

- Direct Plan: Higher NAV (Net Asset Value)

- Regular Plan: Slightly lower NAV

It’s the same fund, but your returns differ based on the route you choose.

Who Should Invest in Direct Plans?

Direct plans are ideal if:

- You understand mutual fund basics

- You’re comfortable doing your own research

- You want maximum returns

- You prefer using digital tools or platforms

Investors using modern platforms often lean toward direct plans for better cost efficiency.

Who Should Choose Regular Plans?

Regular plans make sense if:

- You’re a beginner

- You need financial guidance

- You prefer someone to make decisions for you

- You’re not confident in selecting funds

Here, the extra cost pays for convenience and advice.

Pros and Cons of Direct vs Regular Plans

Direct Plans

Pros:

- Lower cost

- Higher returns

- Full control

Cons:

- No expert guidance

- Requires research

Regular Plans

Pros:

- Professional advice

- Easier for beginners

Cons:

- Higher fees

- Lower returns over time

How to Switch Between Plans

You can switch from regular to direct but it’s treated as a redemption and reinvestment.

Things to keep in mind:

- Exit load may apply

- Capital gains tax may apply

So timing matters.

Final Verdict: Which is Better?

There’s no one-size-fits-all answer.

- If you value higher returns and independence → Direct Plans win

- If you value guidance and simplicity → Regular Plans work better

But here’s the honest takeaway:

With growing awareness and access to tools, more investors today are shifting toward direct plans.

And if you're using a mutual fund investment platform in India, you already have the tools to make smarter, cost-efficient decisions.